The EU Omnibus review of the Corporate Sustainability Reporting Directive (CSRD) introduces significant changes that will reshape sustainability reporting for companies across Europe. Approved by the European Parliament in April 2025, this legislative package aims to simplify requirements, reduce burdens, and provide more apparent timelines for compliance, both in the short- and long-term. These reforms signal a recalibration of the EU’s expansive sustainability agenda to better balance ambition with the practical realities of implementation.

Key changes and impacts of the Omnibus Review on CSRD

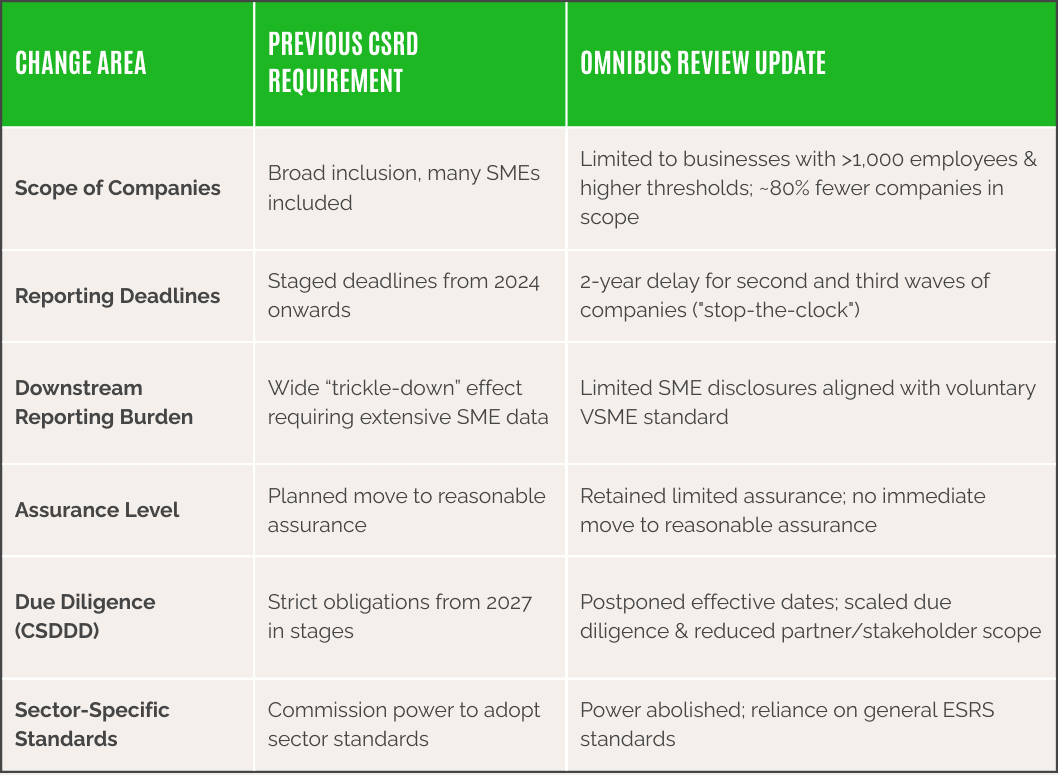

The Omnibus review streamlines the CSRD scope by narrowing the number of companies subject to mandatory sustainability reporting. Notably, the threshold for inclusion now focuses on larger enterprises with more than 1,000 employees and specific turnover or balance sheet criteria, excluding roughly 80% of companies initially slated for coverage. This reduction alleviates compliance pressure on smaller entities, while maintaining robust transparency for major players.

Another significant adjustment is the delayed timeline (‘stop-the-clock’ mechanism) that shifts compliance deadlines for second and third waves of companies by two years. This provides affected businesses with more preparation time and aligns deadlines with the ongoing reforms of the European Sustainability Reporting Standards (ESRS).

The review also limits the ‘trickle-down effect’— the scope of ESG data requests endured by smaller companies through value chains. Small and mid-sized companies will now only have to disclose data proportionate to a new voluntary reporting standard for SMEs (the VSME), preventing excessive burdens on companies not directly covered by CSRD.

Assurance requirements have also been relaxed. The Omnibus removes plans to move to reasonable assurance for sustainability reports, retaining limited assurance instead, with the delayed introduction of EU-wide assurance standards. Additionally, amendments to the Corporate Sustainability Due Diligence Directive (CSDDD) provide relief through postponed effective dates and scaled-back due diligence obligations, encouraging smoother compliance.

Short-term implications

- Extended preparation time: Delays in reporting deadlines help companies avoid rushed implementation, allowing more time to integrate systems and processes for sustainability disclosures.

- Reduced scope: Many smaller companies that would previously have been included are now exempt, lessening immediate compliance obligations and administrative load.

- Clarity on expectations: Clearer limits on downstream reporting requests help businesses anticipate and meet only necessary data demands from supply chain partners.

Long-term implications

- Focused reporting on larger actors: European sustainability efforts will concentrate on entities with the greatest environmental and social impacts, enhancing the quality and comparability of disclosed information.

- Increased SME voluntary reporting: SMEs can adopt new voluntary frameworks such as the VSME standard, encouraging gradual adoption of sustainability reporting aligned with their capacity and stakeholder demands.

- Ongoing evolution of standards: Harmonisation with future ESRS revisions and assurance frameworks will continue, driving a convergence of sustainability and financial reporting over time.

- Enhanced competitiveness: By easing regulatory burdens while maintaining transparency, the Omnibus revision aims to safeguard the competitiveness of European companies amid global ESG expectations.

What companies should do now

Companies need to reassess their CSRD compliance strategies in light of these new rules. Larger firms meeting new thresholds should continue to prepare for full CSRD reporting, while smaller suppliers can explore voluntary frameworks, such as VSME, to meet demand efficiently. The extended timelines offer a welcome opportunity to develop robust systems and enhance data quality. Ultimately, the Omnibus review walks a fine line between maintaining the EU’s ambitious sustainability goals and ensuring companies remain competitive and adaptable in the evolving ESG landscape.

By aligning reporting obligations with company size and capacity — and encouraging phased adoption — this revision sets the foundation for a more inclusive, scalable, and business-friendly approach to European sustainability reporting. Companies that position themselves now for these changes will be best equipped to meet the evolving demands of investors, customers, and regulators alike.